In the vast landscape of global commodities, few elements are as indispensable yet overlooked as molybdenum. Often referred to by metallurgists as the “industrial vitamin,” molybdenum (chemical symbol Mo, atomic number 42) is rarely the star of the show on its own. Instead, it acts as a critical additive that transforms ordinary materials into extraordinary ones. From the skyscraper-reaching alloys of Manhattan to the high-performance turbines of next-generation jet engines, molybdenum is the silent force providing the strength, heat resistance, and durability required for modern civilization.

As we navigate the complexities of the 2026 global economy, understanding molybdenum is more crucial than ever. It is a strategic metal tied to the fortunes of the energy, aerospace, and defense sectors. This comprehensive guide explores the multifaceted world of molybdenum—from its unique chemical properties and global trading hubs to the environmental challenges of its extraction.

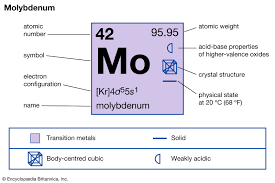

1. The Anatomy of Molybdenum: Properties and Importance

Molybdenum is a silvery-white transition metal that sits in Group 6 of the periodic table. While it does not occur as a free metal in nature, its refined form possesses a suite of physical and chemical traits that make it irreplaceable in heavy industry.

Chemical and Physical Profile

The most defining characteristic of molybdenum is its refractory nature. It belongs to a small elite group of metals known for their extreme resistance to heat and wear.

-

Melting Point: Molybdenum has one of the highest melting points of any element at 2,623°C (4,753°F). This is surpassed only by a few elements like tungsten and tantalum.

-

Density: At 10.28 g/cm³, it is significantly denser than iron, contributing to the structural integrity of the alloys it inhabits.

-

Thermal Expansion: It has a remarkably low coefficient of thermal expansion. This means that when molybdenum is heated, it maintains its shape and size better than most metals, a critical factor for precision engineering in aerospace.

-

Corrosion Resistance: Molybdenum is highly resistant to corrosion by many acids, liquid metals, and glass. In stainless steel, even a small percentage of molybdenum (typically $2\%$ to $3\%$) dramatically improves resistance to “pitting” in chloride-rich environments like seawater.

Why It Matters

Molybdenum’s value lies in its ability to form stable carbides in steel. When added to iron, it increases hardenability, strength, and toughness. Without it, the high-pressure pipelines that transport oil and gas would crack, and the stainless steel used in chemical plants would dissolve under the strain of corrosive reagents.

2. Where Molybdenum Trades: The Global Exchanges

Unlike gold or copper, which are household names in the trading world, molybdenum is a specialized commodity. However, its pricing is a vital indicator for the global steel industry.

The London Metal Exchange (LME)

The London Metal Exchange (LME) is the primary global hub for molybdenum trading. The LME offers “Molybdenum Roasted Molybdenum Concentrate” (Moly Oxide) futures. These contracts allow producers and industrial consumers to hedge against price volatility.

-

Contract Size: Standard LME contracts are for 6 metric tonnes.

-

Pricing Basis: Prices are typically quoted in US Dollars per kilogram or per pound of contained molybdenum.

Regional Markets

Beyond the LME, a significant portion of molybdenum is traded through direct long-term contracts between miners and steel mills. In China, the world’s largest consumer, domestic prices are often influenced by local exchanges like the Shanghai Futures Exchange (SHFE), which tracks stainless steel and ferro-alloys closely related to molybdenum demand.

3. The Geography of Mining: Sources and Major Players

Molybdenum is not found in its pure form. Its primary source is the mineral molybdenite ($MoS_2$). Interestingly, molybdenum is often mined as a by-product of copper mining, though dedicated “primary” molybdenum mines also exist.

Where It Is Mined

The global supply of molybdenum is highly concentrated. In 2026, over 90% of the world’s production comes from just five countries:

-

China: The undisputed leader, accounting for roughly 45% to 50% of global output. Most Chinese production comes from primary mines in provinces like Henan and Shaanxi.

-

Chile: The second-largest producer. Here, molybdenum is primarily a by-product of the massive copper mines in the Andes.

-

United States: Significant production comes from primary mines like Climax and Henderson in Colorado, as well as by-product recovery from copper mines in Arizona and Utah.

-

Peru: A growing force in the market, largely due to increased by-product recovery from its expanding copper sector.

-

Mexico: Maintains a steady output, primarily as a copper by-product.

The Titans of the Industry

The “Big Three” companies that dominate the molybdenum landscape are:

-

China Molybdenum Co., Ltd. (CMOC): A global giant with operations spanning China and Africa.

-

Freeport-McMoRan (FCX): The premier U.S. producer, operating both primary and by-product mines.

-

Codelco: The Chilean state-owned copper company, which produces vast amounts of molybdenum as a secondary stream.

4. Global Trade Flows: Importers and Exporters

The movement of molybdenum across borders is a dance between resource-rich nations and industrial powerhouses.

The Exporters

-

Chile and Peru: These South American nations are the world’s leading exporters of molybdenum concentrates. Because they lack the massive domestic steel capacity of China, they ship the majority of their ore to Europe and Asia for processing.

-

United States: A major exporter of high-purity molybdenum products and roasted concentrates.

-

The Netherlands: Interestingly, the Netherlands often appears as a top “exporter.” This is due to the Port of Rotterdam and major roasting facilities that process imported ore and re-export it throughout Europe.

The Importers

-

China: Despite being the largest producer, China is often a net importer or a “swing” consumer. Its massive domestic infrastructure and manufacturing sectors consume nearly 40% of global supply.

-

Japan and South Korea: These nations lack domestic mines but have world-class specialty steel industries that require huge volumes of molybdenum for automotive and electronics manufacturing.

-

Germany: The heart of European engineering, Germany imports molybdenum primarily for its high-end automotive and machine-tool sectors.

5. Industrial Applications: Where the Metal Meets the Road

Molybdenum’s unique properties allow it to thrive in environments where other metals would fail.

The Steel Industry (The 80% Stake)

Approximately 80% of all molybdenum produced is used in steelmaking.

-

Structural Steel: Used in skyscrapers and bridges to reduce weight while maintaining strength.

-

Stainless Steel: Specifically the “316” grade, which contains molybdenum to resist salt-water corrosion.

-

Tool Steels: Used for high-speed drills and cutting tools that must stay sharp even when red-hot.

Aerospace and Defense

In jet engines, molybdenum-based alloys are used for turbine blades and exhaust nozzles. Its ability to withstand temperatures exceeding 1,000°C without losing structural integrity is a life-saving necessity in flight.

The Green Energy Transition

Molybdenum is a “critical mineral” for the 2026 energy landscape:

-

Wind Turbines: Used in the high-strength steel of the towers and the gearboxes.

-

Solar Panels: Molybdenum is used as a back-contact layer in CIGS (Copper Indium Gallium Selenide) thin-film solar cells.

-

Nuclear Power: Its high melting point and radiation resistance make it ideal for cladding and structural components in reactors.

Catalysts and Lubricants

In the chemical industry, molybdenum is a key catalyst for desulfurization in oil refining, helping produce cleaner-burning fuels. As a lubricant ($MoS_2$), it provides “dry” lubrication in space vacuums or high-load industrial gears where oils would evaporate or fail.

6. Market Dynamics: What Drives the Price?

The price of molybdenum is notoriously volatile, often described as a “lagging indicator” of global industrial health.

Factors Impacting Price

-

Steel Production Cycles: Since the majority of Mo goes into steel, a slowdown in Chinese construction or global automotive manufacturing leads to immediate price drops.

-

By-Product Supply: Because much of the Mo supply depends on copper mining, if copper prices fall and mines reduce activity, the supply of molybdenum inadvertently shrinks, potentially driving Mo prices up even if demand is stagnant.

-

The “Energy” Factor: High oil and gas prices drive investment in new pipelines and offshore rigs, which are heavy users of molybdenum-alloyed steel. This “energy-led” demand can decouple Mo prices from the broader steel market.

-

Geopolitics: Trade tensions between the US and China can disrupt supply chains, as China controls such a massive portion of the primary processing capacity.

7. The Environmental Cost of “The Industrial Vitamin”

No commodity comes without an environmental footprint. Molybdenum mining and processing present specific challenges that the industry is racing to address in 2026.

Mining Impact

-

Tailings Management: Molybdenum mining produces vast amounts of waste rock (tailings). If not managed in secure dams, these can leak heavy metals into local groundwater.

-

Water Intensity: Processing molybdenite ore requires significant water for flotation—a challenge in arid mining regions like North Central Chile or the American Southwest.

Processing and Emissions

-

Roasting: To turn molybdenum concentrate ($MoS_2$) into usable molybdenum oxide ($MoO_3$), the ore must be “roasted” at high temperatures. This process releases sulfur dioxide ($SO_2$). Modern facilities must use sophisticated “scrubbers” to capture these emissions and convert them into sulfuric acid to avoid acid rain.

-

Energy Use: The high-temperature smelting and refining of refractory metals are energy-intensive. As the world moves toward Net Zero, miners are under pressure to transition these processes to renewable energy sources.

Conclusion: The Future of Molybdenum

As we look toward the remainder of the 2020s, molybdenum is poised to remain a cornerstone of the global economy. Its role in the “twin transitions”—digitalization and decarbonization—is secure. Whether it is reinforcing the steel of a hydrogen fuel tank or ensuring the longevity of a deep-sea cable, molybdenum’s unique chemical “fingerprint” makes it a commodity that the world simply cannot do without.

For investors and industry watchers, the key will be monitoring the balance between China’s domestic consumption and the emergence of new green-tech applications. Molybdenum may be the “vitamin” of the industry, but in the 21st century, it is increasingly becoming the essential medicine for a sustainable industrial future.